The Connector Industry – The View From Inside

A close look at prices, material costs, and other major factors, from the people who run the businesses

Periodically, we have discussions with industry leaders to find out what is happening in the marketplace. In recent sessions, we discussed pricing, lead times, raw material costs, and regional and market sector performance.

The following is what we learned from a number of executives at top connector companies.

Pricing

There is not significant pressure for price concessions from the market. Most managers said that this is a fairly normal year for pricing with no large push for price reductions. Most expect prices to remain stable throughout 2012.

Consensus opinion: There will be no meaningful price erosion in 2012. Conversely, price increases are “off the table” this year.

Lead Times

Customers, and especially distributors, are becoming more cautious both in the quantity to be purchased and the frequency of the orders. Most agree that this is a function of softer year-over-year demand for electronics and the current malaise of global economies.

Consensus opinion: Lead times are getting shorter and will probably move from the current six weeks average lead times to five weeks or slightly less.

Raw Materials

Costs have stabilized when it comes to such important raw materials as copper, gold, oil, and plastics.

Consensus opinion: Raw material costs will remain stable for the rest of the 2012 and will not have a negative impact on industry profits.

Market Sectors

The markets identified as performing poorly include consumer, military, industrial, and telecom, particularly wireless infrastructure. The markets doing well include automotive, transportation (non-auto), computer/peripheral, and commercial aviation.

Consensus opinion: Consumer, industrial, and telecom will probably remain at current levels of demand through the third quarter of 2012. Most expect these markets to gain modest momentum in the fourth quarter. Regardless, these markets will end the year with declines in YOY sales. The military market will probably remain at current levels through 2012, meaning no marked improvement in demand and a decline in YOY sales.

Most predict that the European automotive and transportation markets will slow in the second half. North American automotive demand will remain good in the second half, and China will improve.

Geographic Region

Most agree that Europe will not achieve growth in the second half, and many expressed concern about further potential softening. North America is expected to remain at current levels of demand. Japan is slowly doing better and recovering from its 2011 earthquake and tsunami disaster.

China is the big disappointment, with year-over-year sales slightly down through the first half of 2012. The general consensus is for a market pickup in demand in the second half.

Second Half Outlook

Connector industry sales were down low single digits in the first half. Most believe that the industry will be flat sequentially in the third quarter to the second quarter, but will achieve modest improvement in the fourth quarter. Bishop’s forecast is for full year 2012 growth of +3.5%. The executives we spoke with believe the full year 2012 will result in a year-over-year sales decline of low single digits.

The headwinds include: slowing world GDPs (especially in Europe and China); increasing value of the dollar to the euro (we measure the industry in dollars); lack of growth in China, slowing growth in India; a mixed bag of results in Asia, slowdown during the European vacation season, and seasonal pauses as models change in the automotive industry. A significant business headwind is the US November election, which is probably causing many business decision-makers to take a cautious wait-and-see attitude on investment and employment.

The tailwinds include continued strong demand for speed and bandwidth in telecommunications and strong growth in automotive, transportation, and commercial aviation markets. Easy comparisons to 4Q11 will also help with the year-over-year comparison.

Consensus Outlook

Business is OK, displaying neither a tendency for a steep downturn or upturn. However, the bias among the industry leadership is for a slight further softening of demand. Currently, business is holding at existing levels, which is slightly below last year.

As one executive said, “This is a year to hunker down, take a cautious approach to spending (particularly hiring), fix your internal problems, and provide A+ service to your customers.”

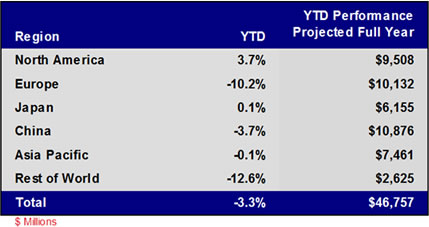

The following chart shows, by region, the year-to-date connector industry performance and what the sales would be if the year ended at today’s performance levels.

No part of this article may be used without the permission of Bishop & Associates Inc.

If you would like to receive additional news about the connector industry, register here. You may also contact us at [email protected] or by calling 630.443.2702.

- Is the Gold Rush Over for China Connector Sales? - October 17, 2023

- The Top Five European Connector Suppliers for Product Quality and Price Competitiveness - October 10, 2023

- 2023 Top Five European Connector Suppliers - September 26, 2023