Renewable Energy – An Industry in Turmoil

Renewable Energy – An Industry in Turmoil

We have been besieged by stories of misfortune and turmoil in the solar and wind industry, caused by overcapacity, regulatory issues, US sequestration, bankruptcies, and the lure of other cheap energy solutions. While this news has been unsettling, it also indicates a healthy shakeout is coming to the renewable energy industry.

If the renewable energy industry continues to follow the evolutionary path that other industries have followed, it appears that 2013 may be another difficult year for manufacturers. While still subject to the effect of changes in the economy, politics, and technology, the industry is following the same patterns as those previously studied, such as the automobile and the semiconductor industry. These established industries have experienced their share of upheaval, and ultimately, the companies who dominated via superior innovation survived the shakeout.

Remarkable technology improvements, cost reductions, and manufacturing economies of scale have spurred the dramatic growth of renewable energy markets over the past decade. The renewable energy industry is entering a transformational stage and is expected to rebound from the shakeout over the next five years.

Solar Energy Update

When analyzing solar photovoltaic (PV) demand, some people refer to installations, while others refer to connections. Global PV installations increased almost 31GW in 2012; however, grid-connected PV amounted to just over 27GW. Connections were lower than installations, owing to lengthy delays in connecting major projects in several countries. For example, in China, up to 2.5GW of PV projects were completed — but not yet connected to the grid — at the end of 2012. Taking a broad look at the solar industry, overcapacity was a significant issue in 2012 and will continue to be throughout 2013.

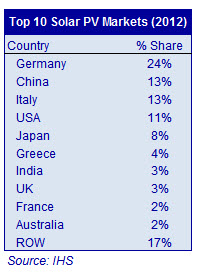

Despite an environment of declining incentives during 2012, Europe remained the largest regional solar market, with slightly more than 17GW of PV demand. European countries accounted for 60% of world demand in 2012, down from 68% in 2011, its first decline since 2006. Looming anti-dumping measures against Chinese manufacturers are taking their toll on Europe, resulting in price increases and additional registration paperwork that will further temper solar demand this year. Almost all of Europe’s “mature” PV markets are predicted to decline in 2013, potentially falling to an overall low of 13GW.

Despite an environment of declining incentives during 2012, Europe remained the largest regional solar market, with slightly more than 17GW of PV demand. European countries accounted for 60% of world demand in 2012, down from 68% in 2011, its first decline since 2006. Looming anti-dumping measures against Chinese manufacturers are taking their toll on Europe, resulting in price increases and additional registration paperwork that will further temper solar demand this year. Almost all of Europe’s “mature” PV markets are predicted to decline in 2013, potentially falling to an overall low of 13GW.

The second-largest region for solar PV demand in 2012 was Asia (including China), with almost 9GW. This region was stimulated by the growth of the Chinese end-market during the second half of 2012. There were nine Chinese firms in the top 15 ranking for solar cell production, and 11 Chinese firms were on the solar modules top 15 list.

Some market analysts are predicting that Japan may grow up to 120% (5GW) in 2013. Mega-solar projects (≥2MW) have been driving Japan’s recent high growth, but this trend should be short-lived once the pipeline for approved projects is complete. To achieve this level of growth, Japan will have to open its market to “foreign” module manufacturers, rather than solely relying on the production capacity of Japanese module manufacturers.

The Americas region provided more than 13% (4GW) of global PV demand in 2012. A large portion of PV demand came exclusively from California, driven by renewable portfolio standards (RPS) and rebates. The US alone had a record installation of 3.3GW of PV. Utility-scale installations represented more than half of new capacity added, totaling 1.8GW. The US is forecast to install at least 3.3GW in 2013, with a potential of nearly 5GW if project installations are completed ahead of schedule.

Worldwide solar PV cell production reached 32.7GW in 2012, while global module production totaled 36.2GW, representing an overall 2% fall from 2011 production levels — the first year-on-year decline in the industry’s history. From a regional perspective, 63% of cells and 64% of modules came from mainland China in 2012. Yingli Solar is also the top cell manufacturer in 2012, followed by JA Solar, Trina Solar, Suntech, and Motech. Thin-film PV lost more ground to silicon PV in 2012, totaling 11% of technology market share, down from 14% in 2011.

Solar Industry

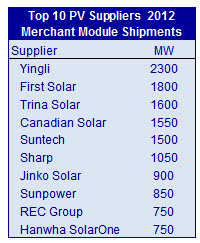

In 2012, the top 10 module suppliers achieved a combined share of 40% of global module shipments, down from 46% in 2011. While the positions in the final standings vary, depending on the industry market analyst, the key players remain the same. Yingli (China) became the largest global supplier of PV modules in 2012, increasing shipment volumes by 43%. First Solar held its position as the No. 2 module manufacturer, while Suntech fell to No. 5 behind Trina Solar and Canadian Solar. REC, the only top-10 supplier in Europe, grew faster than most of its Chinese competitors in 2012, increasing its module shipments by 31% year-over-year.

In 2012, the top 10 module suppliers achieved a combined share of 40% of global module shipments, down from 46% in 2011. While the positions in the final standings vary, depending on the industry market analyst, the key players remain the same. Yingli (China) became the largest global supplier of PV modules in 2012, increasing shipment volumes by 43%. First Solar held its position as the No. 2 module manufacturer, while Suntech fell to No. 5 behind Trina Solar and Canadian Solar. REC, the only top-10 supplier in Europe, grew faster than most of its Chinese competitors in 2012, increasing its module shipments by 31% year-over-year.

In recent years, it was sufficient for the leading module suppliers to focus on a few key markets in the world in order to maintain a successful business. However, as a reaction to the shifting of global installation volumes away from Europe, the strategies of top players are increasingly branching out to emerging regions. For example, Jinko is building a strong presence in South Africa. Canadian Solar generated 26% of its 2012 sales in the US market and is one of the strongest imported brands in Japan. First Solar is focusing on the Latin America market with the acquisition of a Chile-based developer.

In 2012, Germany remained the largest of the world’s top three utility-scale solar photovoltaic markets. China has worked its way up to a very close second and the US is a distant third. The Japanese market is predicted to experience a 120% growth spurt in 2013, with 5GW installed capacity.

The supplier base for PV inverters continued to fragment in 2012. Overall, the market share of the 10 largest PV inverter suppliers decreased from 62% in 2011 to 56% in 2012. Growing demand in Japan and China is cited as the main factor behind the figures, as these are countries where the largest inverter companies have a limited presence. SMA Solar Technology held onto the top position of inverter supplier rankings, but its share of the global market fell for the third year in a row, to just over 25%. In 1Q13, ABB made its move to become the dominant PV inverter specialist with the planned acquisition of No. 2 market leader, Power-One.

Solar Funding and Venture Capital Investments Fall, While PV Module Prices Rise

In 2012, the global average module price decreased by 42% from 2011. In 1Q13, PV module prices actually rose for the first time in four years, and are expected to continue growing by an average of 4% through June 2013. The upswing in prices is attributed to the volume of modules being sold in China and Japan’s thriving markets. Modules today account for less than 20% of a solar system’s cost. While small increases should help stabilize the average selling price (ASP) in 2013, market analysts predict that most leading module companies will not return to profitability until late 2014.

Moving forward, solar generation competitiveness gains will likely come from other parts of the cost structure, such as customer acquisition and permitting.Further fragmentation of the supply chain for PV modules and balance-of-system components is expected across a range of addressable markets due to shifts in geographic access, new and ongoing import trade barriers, and changes in PV application segments.

The solar industry is at the bottom of the cost curve, with little cost left to carve out of solar panels. Much of the research and development activity is focused on improving efficiency by producing more power per panel. Typically, higher efficiency means revenues go up, margins move in a positive direction, and levelized cost of energy (LCOE) goes down.

Consolidation and Specialization Will Emerge in 2013

The solar industry has already experienced consolidation and the trend is expected to accelerate in 2013 with the absorption of assets by larger solar companies, fewer all-in-one corporations, and a more widespread distribution of supply chain services. Although pricing and the cost competiveness of solar PV is improving, almost every policy or incentive driving PV demand has been adjusted to reflect new economics in every major solar-producing country. PV- specific incentives, renewable energy targets, prioritizing solar PV over other renewable energy types, and the willingness of dominant utility suppliers remain the key issues at every country level.

Solar PV installations are forecast to increase 7-12% (31-35GW) in 2013. Emerging markets will help stabilize the solar industry as the developed markets in Europe and the US deal with the elimination of critical incentives. Most of the projections for 2013 put Japan as No. 4 behind China, the US, and Germany. While the number of gigawatts installed will increase compared to last year, it will not be enough to absorb all of the overcapacity. The gap between solar PV supply and demand narrowed slightly in 2012, but overcapacity will continue to weigh on the industry for the next several years.

Wind Energy Update

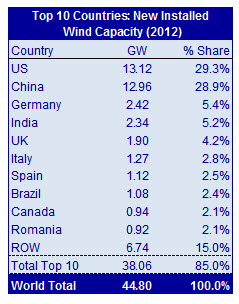

A record 44.8GW of new wind power was installed globally in 2012, 10% more than 2011. Cumulative global wind power capacity reached 282.5GW in 2012, an increase of about 19% compared to 2011. While these numbers are certainly positive, a wave of uncertainty has enveloped the wind industry, as many global  governments try to manage their economic crisis by altering or reducing their support for renewable energy projects. Investors look for long-term stability, and the high amount of policy changes being made are making it more difficult for wind farm developers to get the financing they need.

governments try to manage their economic crisis by altering or reducing their support for renewable energy projects. Investors look for long-term stability, and the high amount of policy changes being made are making it more difficult for wind farm developers to get the financing they need.

The US claimed the top spot for global markets in 2012 for the first time since 2009. In a last-minute rush to beat the anticipated expiration of the Production Tax Credit (PTC) at the end of December, the US installed more than 8GW in 4Q12, finishing up at 13.1GW for the year. Canada had a solid year, and Mexico more than doubled its installed capacity. Unfortunately, due to the late extension of the PTC in January, a US market slowdown is anticipated in 2013.

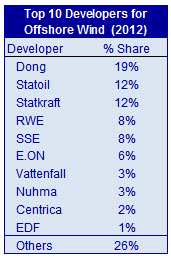

European markets, led by Germany and the UK, accounted for 12.4GW last year, a new record. Europe also continued to lead the offshore wind markets, with 1.2GW installed, more than 90% of total offshore installations of 1.3GW in 2012. Due to policy uncertainty, Europe’s record installations are unlikely to be repeated in 2013.

European markets, led by Germany and the UK, accounted for 12.4GW last year, a new record. Europe also continued to lead the offshore wind markets, with 1.2GW installed, more than 90% of total offshore installations of 1.3GW in 2012. Due to policy uncertainty, Europe’s record installations are unlikely to be repeated in 2013.

Both the Chinese and Indian markets slowed down in 2012, with their annual installations coming in at 13.2GW and 2.3GW respectively. China is the world’s largest market, with more than 75GW of total installed capacity and another 18 GW forecast for 2013. The wind industry in India went through a yearlong policy hiatus and is expected to return to growth in 2014. Emerging markets are expected to drive global growth during the next five years.

New offshore wind capacity increased by one-third last year, 90% of which was in European waters. Just less than 1.3GW of offshore capacity came online in 2012. Ten developers accounted for more than 70% of last year’s new European offshore capacity. Based on projects under construction, total European capacity is forecast to reach 8.3GW by the end of 2014. China and Japan are also expected to develop significant offshore wind assets in the long term.

Wind Industry

The top 10 turbine suppliers of 2012 in order were: GE (US), Vestas (Denmark), Siemens (Germany), Enercon (Germany), Suzlon (India), Gamesa (Spain), Goldwind (China), United Power (China), Sinovel (China), and Mingyang (China). Goldwind and Sinovel slid down the rankings in 2012, due to a 26% decrease in Chinese installations, transmission bottlenecks, and manufacturing overcapacity in the Chinese OEM home markets.

Driven by policy uncertainty, merger and acquisition activity in the wind energy sector spiked in 2012, while VC funding decreased slightly. There were 35 acquisitions in the wind energy sector in 2012, more than double the 17 acquisitions seen in 2011. Market uncertainty took its toll on investment last year, as VC funding in the wind energy sector was slightly lower than in 2011.

Advances in wind turbine technology have boosted capacity factors over the last few years. Taller towers that reach stronger wind resources, along with longer blades that capture more energy, translate into lower overall cost of wind-generated electricity. With longer blades, larger rotors, and high hub heights, wind energy is now viable in places previously thought unworkable. Wind technology is also revisiting smaller turbines and vertical-axis turbines for rural applications.

Wireless technology continues to be explored as an alternate means to get data from the nacelle to the ground. For critical turbine control systems, however, it will still be necessary to rely on the high communications performance and reliability of wired networks. This follows the trend seen in other industries, where wireless technology makes new connectivity possible but does not replace existing critical infrastructure.

GE announced a new 2.5MW turbine with a 120-meter rotor diameter specialized to low-wind regions. GE calls it the first “brilliant” turbine because of a 25% increase in efficiency that will increase power output by 15%. The new wind turbine series uses electrical system upgrades and the power of the industrial Internet to connect data points across the turbine’s ecosystem, and allows for higher energy capture in lower wind-speed environments.

Wind Market’s Gradual Recovery

The wind industry managed to evade what could have been a disastrous year by securing a one-year extension of the US PTC. Unfortunately, the extension came too late for many firms to resurrect their development plans for 2013. Wind power installations are projected to drop by almost 7% in 2013, compared to 2012. It will be especially tough for manufacturers, with an oversupply of turbines adding to existing downward price pressure to cut margins. Growth in Asia Pacific, Latin America, Northern Europe, the Middle East, and Africa will offset some of the declines in the developed wind regions, which are experiencing some degree of policy uncertainty. A modest market recovery is anticipated in 2014, with continued growth at an average rate of 13.7% to 2017.

Renewable Energy Outlook

Currently, the use of renewable energy is still limited, in spite of its vast potential. Financial incentives from governments around the world provided the impetus for a growing, wholesale shift away from fossil fuel energy to the development of clean, renewable energy resources.

In the future, the energy business is likely to be one of customer choice. Energy conservation will be the matter-of-fact way in which people live their lives. Owning the means of renewable energy production will be viewed as a hedge against escalating energy prices and a deteriorating environment. In order for renewable energy to survive, continued innovation is required, but innovation and manufacturing cost money.

Industry consolidation, bankruptcies, improved technology innovation, and improved economies should ultimately lead to a stronger, prosperous supply chain. The key going forward will be to address these new market challenges and continue policies that help renewable energy technology to grow sustainably, continuing its evolution to a mainstream electricity source.

- State of the Industry: 2022-2023 Connector Sales - April 16, 2024

- Amphenol is On a Roll - April 2, 2024

- Nicomatic Proves That Two Heads are Better Than One - March 26, 2024