Facts & Figures: Wireless Continues Upward Trend

Wireless demand impacts I/O connector demand in ways that are hard to count.

Wireless connectivity continues to grow rapidly. From a connector usage standpoint, wireless is a displacement technology; that is, devices that use wireless connection technologies do not necessarily also include a physical connector to perform the same function redundantly. So, if the device is Bluetooth-enabled, it does not require an audio headphone port as well, although many still include them. This is the catch for the connector industry: Eliminate (displace) the connector from the device or not?

The main displacement technologies are Wi‐Fi, Bluetooth, cellular, ZigBee, and wireless charging. Each is defined by the value or unit volume that the technology has now and is projected to have in the future.

Wi-Fi

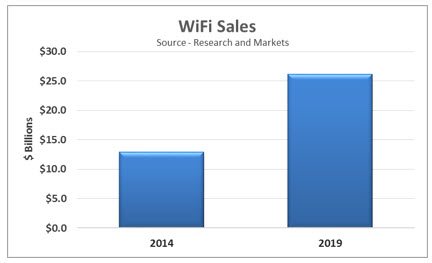

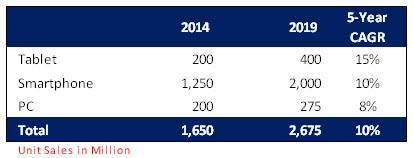

Wi-Fi is being built into most mobile devices. Almost any smartphone, tablet, or mobile computer will have Wi‐Fi built in. Many desktop computers and computer peripherals also have Wi‐Fi built in to simplify networking solutions in the home and office. In home entertainment systems, such as high-definition televisions, Wi‐Fi is also one of the networking options. As reported recently by BusinessWire, Research and Markets has identified the global Wi‐Fi market at a value of $12.9 billion in 2014 with a CAGR of 15.2% that will take the market to $26.2 billion in 2019. In unit volumes, just from smartphones, tablets, and mobile computers, we will see nearly 1,650 billion units in 2014 grow to 2,675 billion units in 2019.

Wi‐Fi will need to grow. Cisco has identified that as mobile cellular traffic grows, more than half the traffic (almost 17 exabytes in 2018) will have to be off‐loaded to Wi‐Fi and femtocells.

Bluetooth

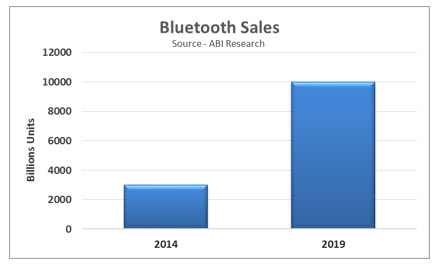

In both its traditional and Smart versions, Bluetooth is also being built into most mobile devices. All smartphones now have Bluetooth along with Wi-Fi. Either technology can be used to pair devices, form a hub, and make connections to other mobile devices. They are also used to pair headsets in automotive infotainment and home automation systems and peripherals. Bluetooth has at least the unit volume potential of Wi‐Fi, plus its low-power version (Smart) can be used in devices that only have a small amount of battery power, particularly in the Internet of Things (IoT). According to ABI Research, more than three billion Bluetooth-enabled devices will ship in 2014. This will grow to more than 10 billion units shipping in 2019, a CAGR of 35.1% over that time period.

WiFore Consulting projects “appcessories,” devices that connect to smartphones and tablets through Bluetooth Smart technology and are intimately linked to apps on these devices, will grow exponentially. This new field of products for the IoT is expected to grow from 51 million devices in 2014 to 13,111 million devices in 2020. The market value to the IC manufacturers reaches almost $6 billion in 2020 and produces revenues for these appcessories of more than $130 billion.

Cellular Networks

Cellular networks will be the long-distance wireless technology for smartphones, tablets, and other enabled devices. According to Cisco, in 2013, the number of devices connected to mobile networks grew to seven billion, up 526 million devices from 2012. In 2018, there will be more than 10 billion mobile devices connected to the mobile network. Fourth‐generation (4G) connections will grow from 2.9% of the connections to 15% of the connections. According to GSMA, in 2013, annual mobile network operator revenues were $1.2 trillion and will grow to $1.4 trillion in 2020.

The market for data communications equipment to support mobile networks is substantial. According to GSMA, since 2008, mobile network operators have spent more than $1 trillion in capital equipment to improve their networks. Capital investment over the six-year period 2014 through 2020, in order to accommodate global data traffic, is forecasted to be $1.7 trillion. And even with this investment, mobile traffic demand will be greater than the mobile network capacity.

ZigBee

ZigBee, based on 802.15.4, is a wireless technology that was aimed at the home automation market. It has been a dominant player in the market, which is expected to exceed 351 million devices in 2018, according to ABI Research. It looks, however, like Bluetooth Smart will likely be the dominant player in home automation, given its dominance in other areas like mobile devices which can control home automation.

Wireless Charging

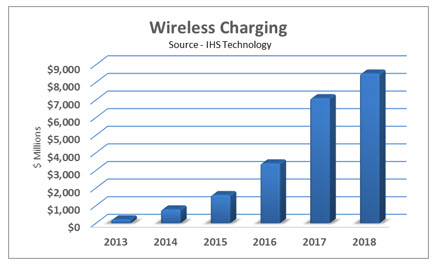

Wireless charging has been around awhile but is now projected to become more popular in mobile devices. According to IHS Technology, the growth will be fueled by the partnership of two main (and previously competing) industry groups which will allow standardization and thereby the growth of mobile devices. Wireless charging was a $216 million market in 2013 and will grow to $785 million in 2014 and $8.5 billion in 2018. This is a five-year CAGR of 108.4%.

In looking at wireless data transfer and wireless charging in mobile devices, the overall market forecast in units for these devices is growing at a five-year compound annual growth rate of 10%. Tablets are growing the fastest at 15%; smartphones have lower growth, but more volume; and laptops have the least growth.

Unit Sales of Mobile Devices, 2014 to 2019

Smartphones are the devices most likely to employ wireless technology and replace (displace) the external I/O connectors because they have the least spare room to accommodate redundancy. Most smartphones currently have two I/O connectors, one audio connector for headphones and a small rectangular connector for power/charging and data. The audio connector is redundant as most smartphones (possibly all) have wireless Bluetooth capability and Bluetooth headphones are readily available. Some smartphones have wireless charging but, until recently, with two competing wireless charging standards, many companies were reluctant to commit. The single standard, which is now being developed, likely will push the smartphone manufacturers to use wireless charging. This will eliminate many of the rectangular connectors and may also eliminate the audio connector to simplify and minimize the dimensions of the phone. Bishop estimates that more than 50% of these I/O connectors will be eliminated in the next five years.

The outcome is less clear for tablets since many have spare real estate for the connectors, but the smaller tablets will tend toward the space-saving option. Bishop estimates that less than 30% of the I/O connectors will be eliminated in the next five years in tablets.

Portable PCs are the least likely to eliminate the I/O connectors. Although all of these PCs have Wi-Fi and Bluetooth, there are few real estate issues to drive their displacement. Higher-speed I/O ports are an advantage for these machines and the I/O connectors are relatively inexpensive. Also, many portable PCs double as desktop computers, and the I/O connectors increase their functional flexibility.

If you would like to read more on wireless connectivity market, see Bishop & Associates, Inc. new report, Evolving Wireless Power and Data Interconnects.

This report examines:

- The basic characteristics of wireless and contactless technology, reviewing advantages and limitations along with examples of typical applications where the technology has been implemented.

- The effect contactless interconnects can have on data rates and system packaging.

- The use of millimeter wave transmission as a possible solution to the looming shortage of available frequency bands.

- Which market sectors will benefit most from wireless and contactless connectivity and how will the Internet of Things spur the evolution of this technology?

[hr]

No part of this article may be used without the permission of Bishop & Associates Inc. If you would like to receive additional news about the connector industry, register here. You may also contact us at [email protected] or by calling 630.443.2702.

- The Outlook for the Cable Assembly Industry in 2021 and Beyond - May 18, 2021

- A Data-Hungry World is Driving Demand for Wireless Connections - January 26, 2021

- Innovation and Expansion Drives Growth of Global Cable Assembly Market - May 7, 2019