Smartphones Get Smarter: Can Networks Keep Up?

The cellular infrastructure business struggling to meet demand.

Bishop tracks 13 market sectors for electronic interconnects sales trends. The combined annual revenue of all the market sectors was $4.3 trillion in 2012 and grew 4.9% over 2011. Of the 13 market sectors, telecom/datacom was the sixth-fastest growing market sector in 2012 at 2.4% year-over-year and combined revenues of $288.7 billion. Profitability was $35 billion at 11.8% of sales.

Bishop tracks 13 market sectors for electronic interconnects sales trends. The combined annual revenue of all the market sectors was $4.3 trillion in 2012 and grew 4.9% over 2011. Of the 13 market sectors, telecom/datacom was the sixth-fastest growing market sector in 2012 at 2.4% year-over-year and combined revenues of $288.7 billion. Profitability was $35 billion at 11.8% of sales.

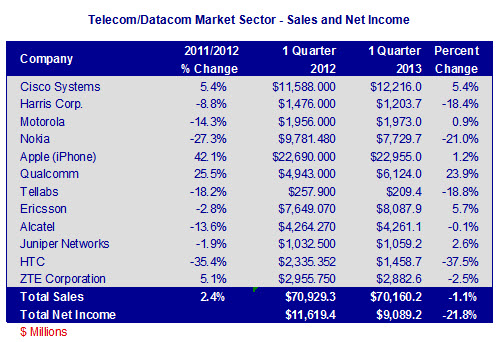

Qualcomm had the most growth in 1Q13 at 23.9% year-over-year to $6.1 billion. Qualcomm designs semiconductor chips that run smartphones and mobile tablets, which resulted in the strong sales growth.

Ericsson and Cisco registered the next-highest growth rates at 5.7% and 5.4%, respectively. Ericsson attributes its growth to new cellular networks and rollout services. Cisco recorded higher sales for its businesses in the United States and in emerging markets. Juniper Networks, another infrastructure equipment company, recorded a small sales increase of 2.6%.

Apple’s iPhone, in comparison to the last two years, had relatively modest sales growth of 1.2% in 1Q13 at $23 billion. Apple’s iPhone has seen increasing competition from Samsung and other smartphone manufacturers.

Nokia and Motorola have both had problems competing in the smartphone market. Both companies experienced double-digit decline in 2012 sales. Nokia, which had been the largest manufacturer of cell phones in the world, had a sales contraction of 21% in 1Q13.

HTC’s revenues declined 37.5% in 1Q13 primarily due to increasing competition in the Android smartphone market.

The following table shows the results for the 12 companies we track in this market sector.

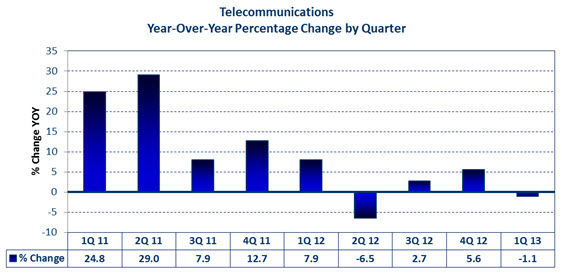

As can be seen in the following chart, year-over-year sales growth slowed down in 2Q12 to a negative level and has bounced up and down modestly the last three quarters. Sequentially, first quarter 2013 sales decreased 18.6% from the fourth quarter of 2012.

Trends in the Telecom/Datacom Industry

- Smartphones are often the smartest piece of equipment in a consumer’s home, besides a PC.

- Smartphone popularity has grown much faster than predicted, increasing the competition for the product and resulting in price erosion for subscriber equipment.

- Increasing use of smartphones has driven up the data use demand on the world’s wireless networks (infrastructure), forcing an increase in the capacity of the systems or replacement with LTE systems that handle the volume more efficiently. At the same time, competition among the service providers is driving down prices and eroding profits, making them less inclined to spend money on capital equipment.

- Emerging countries are moving directly to cellular phone systems and skipping the implementation of landline systems.

Impact on the Cable Assembly Industry

- Subscriber equipment (smartphones/cell phones) tends to use lower-cost flex circuit cabling and the price competition is intense.

- Infrastructure equipment uses more expensive cabling and offers more opportunities to the cable assembly industry.

- Data center and server farms use significant amounts of external cabling and offer good opportunities to the cable assembly industry, particularly for custom installations.

- The final trade-off in cabling requirements, for the switch to mobile data, is yet to be fully understood, as the technology is evolving. Cable types, however, are trending toward miniaturization and flex circuitry.

Bishop & Associates projects the worldwide market for telecom/datacom cable assemblies to grow 4.9% in 2013 to $17.8 billion. North America will be the fastest-growing region in 2013 for this market sector.

No part of this article may be used without the permission of Bishop & Associates Inc.

If you would like to receive additional news about the connector industry, register here. You may also contact us at [email protected] or by calling 630.443.2702.

- The Outlook for the Cable Assembly Industry in 2021 and Beyond - May 18, 2021

- A Data-Hungry World is Driving Demand for Wireless Connections - January 26, 2021

- Innovation and Expansion Drives Growth of Global Cable Assembly Market - May 7, 2019