Big OEM Sales, No Profits: Consumer Market for Cable Assemblies

Big OEM Sales, No Profits: Consumer Market for Cable Assemblies

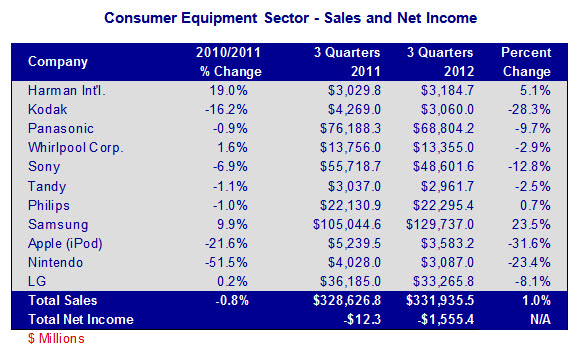

The consumer equipment sector contracted almost 1% in 2011 and net income was 0% of sales. Year-to-date performance for the industry shows very modest growth but a precipitous drop in profitability.

The consumer equipment sector contracted almost 1% in 2011 and net income was 0% of sales. Year-to-date performance for the industry shows very modest growth but a precipitous drop in profitability.

Of the 11 companies tracked in this segment, eight had declining sales year-over-year for the first three quarters. Five of the companies had year-to-date losses totaling more than $19 billion.

- Apple’s sales of iPods declined 31.6% year-to-date compared to the same period in 2011. This is likely the result of some competition, but is also from the iPad and iPhone cannibalizing some of the iPod sales. Its profitability, however, is estimated at a healthy 26% of sales.

- Kodak’s sales declined 28.3% year-to-date, due in part to its continuing slide in the competitive digital camera and printer markets. Its net income is a decidedly unhealthy -32%.

- Panasonic’s sales slid 9.7% year-to-date. They have also accumulated a staggering operating loss of $14 billion or -20.4% of sales. They attribute the problems to a strong yen dampening export sales, the 2011 earthquake/tsunami damaging their supply base, and write-downs from the purchase of Sanyo.

- Sony and Nintendo are both struggling in the gaming console and hand-held markets.

Two of the companies have had good performance year-to-date.

- Samsung’s sales have increased 23.5% year-to-date, in large part due to their Galaxy smartphone and tablet products. Profits are $14.9 billion, up a whopping 59% year-to-date.

- Harman, a supplier of premium audio and infotainment systems, has also done well. Its sales are up 5.1% year-to-date and profits are up 166% to 8.7% of sales.

Year-to-date performance of each of the 11 companies in this sector can be seen in the following table.

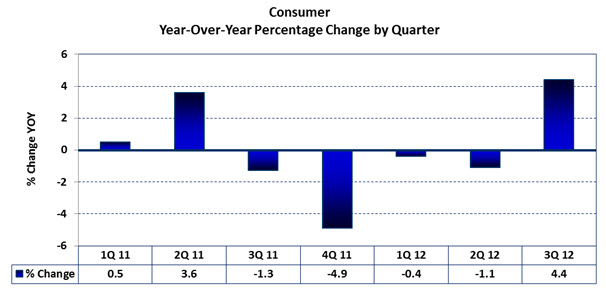

As can be seen in the following graph, year-over-year sales growth returned to the consumer market after four quarters of declining sales. Quarter-to-quarter (3Q12 versus 2Q12) sales increased 6.8%. Five of the 11 companies had a quarter-to-quarter increase in sales.

Although many other factors impact the consumer market, here are some key points:

The recession in Europe is keeping consumer spending muted in that region. Disposable income is in short supply, which impacts impulse purchases such as music players and hand-held gaming devices. The slow housing market in Europe is keeping down purchases of appliances except for replacements.

The subdued consumer spending may extend well into 2013.

In the US, consumer spending has been fairly strong, but it is also changing. Consumers are using the Internet to research products and purchase them at the lowest price. This is one of the factors driving down the profitability on consumer goods.

The US Commerce Department recently found that Samsung, LG, and Electrolux may have been selling their large washing machines in the US at unfairly low prices. The accuser, Whirlpool, would stand to gain an advantage if duties are imposed. Trade rules, in general, may shift the regions in which white goods are manufactured.

Consumer spending in China has been strong. If the recession in Europe grows worse or the US goes into recession, however, this would affect China’s economic growth and, ultimately, its consumers’ paychecks.

Although Brazil does not have a major impact on the world economy, an interesting case study has been developing there. The Brazilian economy has been cooling off for several quarters and is near stagnant conditions. The consumers there, however, have continued to spend. The caveat is that the consumers’ personal debt has skyrocketed over the last few years, as it did in Europe and the US in the 2000s. Is there a burst bubble in their future? Could this happen in China?

Bishop forecasts:

- Cable assembly manufacturers servicing the consumer market are always under pressure to reduce pricing. This pressure will increase as the OEMs seek to return to profitability in 2013.

- The recession in Europe will continue to affect cable assembly manufacturers there. 2013 is expected to be a very flat year in Europe, at best.

- The industry should stay aware of changing trade rules. In white goods, cable assembly manufacturing tends to shift to where the OEMs build the products due to the logistics of shipping these end products.

- The world economy is still very fragile. When the dust settles on 2012, Bishop & Associates expects the worldwide market for consumer cable assemblies to contract by 2.7%, to a worldwide value of $5.9 billion. The best growth rate is expected in Japan. Worldwide growth, in 2013, is expected to be in the range of 3.4%.

- The Outlook for the Cable Assembly Industry in 2021 and Beyond - May 18, 2021

- A Data-Hungry World is Driving Demand for Wireless Connections - January 26, 2021

- Innovation and Expansion Drives Growth of Global Cable Assembly Market - May 7, 2019