The Semiconductor/Interconnect Market Connection

Bishop tracks 13 market sectors for electronic interconnects. The combined annual revenue of all the market sectors was $4 trillion in 2011 and grew 9.7% over 2010. Of the 13 market sectors, semiconductor was the eighth-fastest-growing in 2011 at 8.6% year-over-year and combined revenues of $135.6 billion. Profitability was $21.7 billion at 16.0% of sales.

Bishop tracks 13 market sectors for electronic interconnects. The combined annual revenue of all the market sectors was $4 trillion in 2011 and grew 9.7% over 2010. Of the 13 market sectors, semiconductor was the eighth-fastest-growing in 2011 at 8.6% year-over-year and combined revenues of $135.6 billion. Profitability was $21.7 billion at 16.0% of sales.

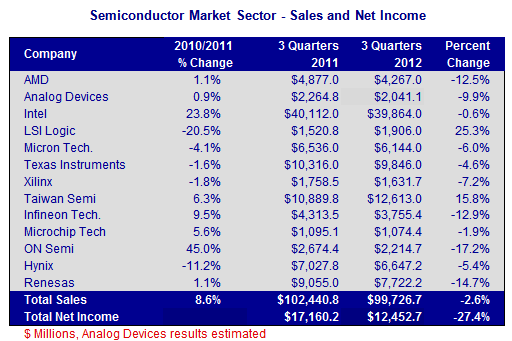

In 2012, sales in the first three quarters were down -2.6% compared to the same period in 2011. Net income is down -19.9% compared to 2011. The decrease is primarily due to the lower volumes and manufacturing utilization.

LSI Corporation recently reported full year 2012 sales up 23% to $2.5 billion year-over-year on continuing operations after contracting -20.5% in 2011. LSI sold its external storage system business in 2012 and is now more focused on semis. The 2012 growth is attributed to its strong position in flash processors, growth of its HDD business, growth of its SAS and ServerRAID products, and major design wins for its Axxia networking products.

Taiwan Semiconductor Manufacturing Company (TSMC), a dedicated semiconductor foundry, does work for several large fabless companies like Qualcomm and Advanced Micro Devices. TSMC’s revenues were up 15.8% year-over-year in the first three quarters of 2012. Sales growth was primarily in its communications products, up 23% in 4Q12, and industrial/standard products, up 42% in 4Q12.

ON Semiconductor has had the worst performance of this group of companies, with a year-over-year decline of -17.2% for the first three quarters of 2012. For the full-year 2012, ON’s communication products were down -19% from 2011, automotive products were down -2%, and the computing end-market products were down -16%.

The following table shows the results for the 13 companies we track in this market sector.

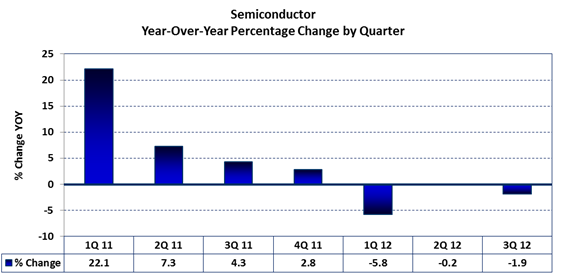

As can be seen in the following chart, year-over-year sales growth has been declining or negative for the past seven quarters. Sequentially, third quarter 2012 sales increased 3.8% from the second quarter of 2012.

Growth Trends of Semiconductor and Interconnect Markets

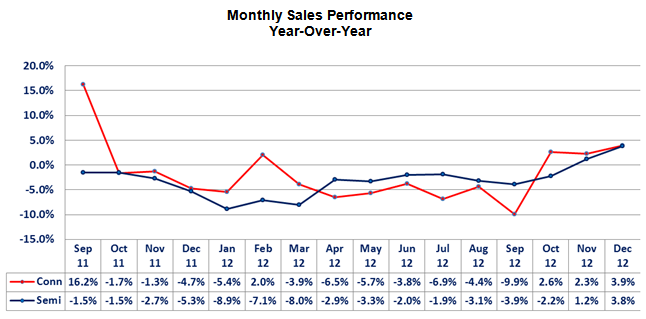

As can be seen in the following graph, the year-over-year growth trends of the semiconductor and interconnect industries closely parallel one another. In 2012, connectors started off a little stronger, but were then overtaken by semiconductors in the April-through-September timeframe. By the end of the year, the differences merged and the last two months were very close. Connectors ended up contracting 2.7% and semiconductors contracted 3.3%.

The following graph shows the comparison of the monthly year-over-year performance of the connector industry versus the semiconductor industry over the last 10 years. At 0.85 for this period, the correlation coefficient between the performances of each industry is very high. The semiconductor line is more muted than the connector line because SIA uses a three-month moving average for their numbers.

Impact on the Cable Assembly Industry

- Although semiconductors do not directly use cable assemblies, in most cases, they are used in equipment that often does employ cable assemblies, so semiconductor sales performance is a good indication of the cable assembly industry performance.

- Semiconductors are projected to grow 4.5% in 2013 by Gartner. Connectors and interconnects are projected by Bishop to grow 4.2% year-over-year in 2013.

- Weak spots for both industries in 2013 will be in low demand for personal computer sales. Areas of strength will be in automotive, smartphones, and mobile computing (such as tablets).

Bishop & Associates projects the worldwide market for cable assemblies to be up 4.3% in 2013 to $124.5 billion. The semiconductor market is projected to reach $304 billion in 2013.

- The Outlook for the Cable Assembly Industry in 2021 and Beyond - May 18, 2021

- A Data-Hungry World is Driving Demand for Wireless Connections - January 26, 2021

- Innovation and Expansion Drives Growth of Global Cable Assembly Market - May 7, 2019