The State of China’s Electronics Market

John MacWilliams makes his predictions for China’s electronics market in the near future.

China will continue to export from massive factories and add capacity to meet burgeoning domestic demand for the foreseeable future. Meanwhile, OEMs are beginning to insource products once again. Products and components built in North America and Europe include higher-value products such as desktop PCs and iMacs, MacBook Pros, servers, base stations, and telecom central office products, as well as existing (but threatened) domestic parts for automotive, appliance, medical, industrial, military/aerospace, and niche applications.

China will continue to export from massive factories and add capacity to meet burgeoning domestic demand for the foreseeable future. Meanwhile, OEMs are beginning to insource products once again. Products and components built in North America and Europe include higher-value products such as desktop PCs and iMacs, MacBook Pros, servers, base stations, and telecom central office products, as well as existing (but threatened) domestic parts for automotive, appliance, medical, industrial, military/aerospace, and niche applications.

Foxconn, one company that is widely associated with China, now has two plants in the US (Texas and Indiana) and one engineering facility. It recently announced a $30 million expansion in Harrisburg, Pa., probably for the manufacturing of Apple products. Going in the other direction, beleaguered RIM (Ontario, Canada) is outsourcing Blackberry production to Foxconn, but not in China; still, a watershed move for the company.

Ordering Spare Parts from China?

Along the way, problems are developing, one of which is spare parts. One example: Consumers may be out of luck if they can’t find replacement parts on eBay. This has led to a disposable mentality towards many goods, in which cheaper goods need to be replaced frequently, ultimately costing more. The volume PCB manufacturing capacity has been decimated in the US, due to environmental concerns and offshore manufacturing. It will be hard to replace that. In addition, the general manufacturing side of the electronics business, as a result of outsourcing, has gone to lower margin suppliers with less financial resources to invest in new plants and equipment. Even the semiconductor industry is having problems keeping up with incredibly expensive advanced fab facilities. This becomes a license to shop elsewhere in the world, perhaps seeking locales where government incentives may be available.

Asia Versus Latin America

Below is a summary of the International Monetary Fund’s forecast comparing Asia to Latin America.

Asia

- China’s hyper-growth cooling to single digits

- China’s manufacturing output turning to internal demand

- Growth limited by a lack of foreign capital

- Reining in loose credit to a more sustainable level

- India expected to rebound to 6% GDP by 4Q14

Latin America

- Brazil lowering exchange rate = stronger investment

- North America insourcing may have mild impact

- South America continues punitive import duties

- Investing in South America oil and mining

- Mexico to benefit from strengthening North American economies

The International Monetary Fund (IMF) forecasts a return to modest growth through 2014 in the developed world and lower, but still positive, growth in Asia. Although not said, if the lessons from this past downturn are taken to heart, and difficult social decisions are made, there are prospects for renewed strong growth from mid-2014 to at least 2017. However, there remain uncertainties, led by the future direction of US fiscal policy and political rapprochement with China. The results of debt and credit policy decisions worldwide are still questionable and could trigger another recession. Look for ~3.5% GDP growth in 2014 in the US, 1% in Europe and Japan, 7-8% in China, and ~3% in Latin America.

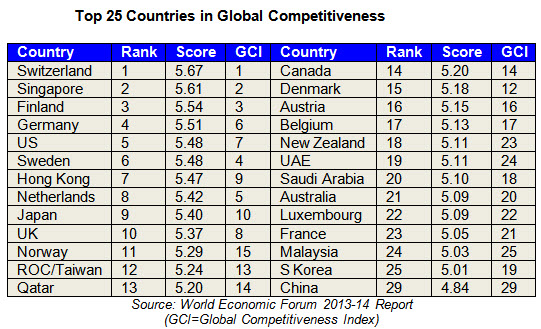

Global Competitiveness Index

The World Economic Forum issues the Global Competitiveness Report by country. The detailed 2013-14 report ranks countries in many different areas, including institutions, education and training, readiness of infrastructure, market efficiency, market size, macroeconomic environment, labor market, business sophistication, financial market development, and innovation.

In the current report, the US ranks 5th overall and 7th in its Global Competitiveness Index (down from 1st five years ago). China ranks 29th, while its neighbor Taiwan ranks 12th.

The key takeaway from this study is that it evaluates a large number of factors, including many that are “social” in nature. It also attempts to define the “sustainable competitiveness” category, in which China ranks 29th out of 147 countries.

China’s Electronics Market Forecast

The migration of manufacturing to China over the past decade was initially met with resistance in Western economies, because when factories in the West closed, workers lost jobs, impacting Western economies. As the full brunt of the global economy began to take hold, there was and is less resistance — and a mad rush by companies to get in on the action. It is hard today to find a consumer item that was not made in China. Thus, there is perhaps a grudging acceptance that much of this movement was unavoidable, that outsourcing is an efficient use of resources, and that it keeps costs down for the ultimate consumer.

In the electronics manufacturing sector, including connectors, decisions are made based on cold hard facts and the profit/ROI motive. One aspect is that connector makers have to manufacture where the demand is, if that is what the customer (OEM, EMS supplier) wants. If Foxconn wants local manufacturing support for its Shenzhen factory, then you manufacture and stock there, even if those end products are then exported back to the US.

Now, the worm may be turning. Whether it is an airbrush routine for mostly China manufacturing, or a real trend, remains to be seen.

One thing that strikes me in this process is how rapidly decisions were made and how quickly China came up to speed with high-volume manufacturing. I’m not sure that could have happened here, given our corporate, consensus-building business culture and all the red tape. Perhaps Terry Gou, president of Foxconn, personifies the rapid decision-making process in China, whether it is up to one man or one government agency.

Another is that in a dangerous world, interdependence is good. Fifty years ago, China was a serious adversary. Its economy is now largely dependent on Western demand. It may be true that Western technology will continue to be our strong suit, so that we export idea-creation and technology while importing the “ditch-digging.” The only problem with that is that we need many fewer knowledge workers than workers on the assembly line. This has contributed significantly to high unemployment rates in developed economies, where fewer unskilled workers are needed, and only some of those with advanced skills can rise to the top.

Read part one of this article, published January 21st.

John MacWilliams, Market Director, Bishop & Associates, Inc.

- Electric Vehicles Move into the Mainstream with New EV Battery Technologies - September 7, 2021

- The Dynamic Server Market Reflects Ongoing Innovation in Computing - June 1, 2021

- The Electronics Industry Starts to Ease Out of China - November 3, 2020